Gradual improvement is anticipated for the nation’s homebuilding and remodeling sectors in the wake of the recent decision by the Federal Reserve to announce the first in what is expected to be a series of interest-rate reductions, housing analysts are predicting. Among the key statistics and forecasts released in recent weeks by government agencies, research firms and industry-related trade associations were the following:

Housing Starts & New-Home Sales

The National Association of Home Builders is forecasting “gradual improvements” for the homebuilding sector as the Fed continues to ease monetary policy, and mortgage interest rates trend lower in the months ahead. “With inflation moderating, the Federal Reserve is expected to begin a cycle of monetary policy easing which will produce downward pressure on mortgage interest rates and also lower the interest rates on land development and home construction business loans,” said NAHB Chief Economist Robert Dietz. A recent rise in single-family building permits is further good news for housing, which was hit hard by tight monetary policy in the first half of 2024, the Washington, DC-based NAHB said. According to the latest available numbers, single-family starts were pacing at a 992,000-unit seasonally adjusted annual rate, up 10.4% year-to-date over 2023. “Thanks to lower interest rates, builders now have a positive view for future new home sales for the first time since May 2024,” said NAHB chairman Carl Harris.

Existing-Home Sales

The recent decision by the Federal Reserve to lower interest rates, coupled with increasing inventory, “is a powerful combination” that will provide the environment for existing-home sales to move higher in future months, according to the chief economist for the National Association of Realtors. According to Lawrence Yun of the Washington, DC-based NAR, although recent existing-home-sales figures have been “disappointing,” housing inventory is up roughly 23% from a year ago, while unsold inventory sits at a 4.2-month supply at the current sales pace, up from 3.3 months at the same time a year ago. “The rise in inventory, and the accompanying months’ supply, implies that home buyers are in a much-improved position to find the right home, and at more favorable prices,” Yun said.

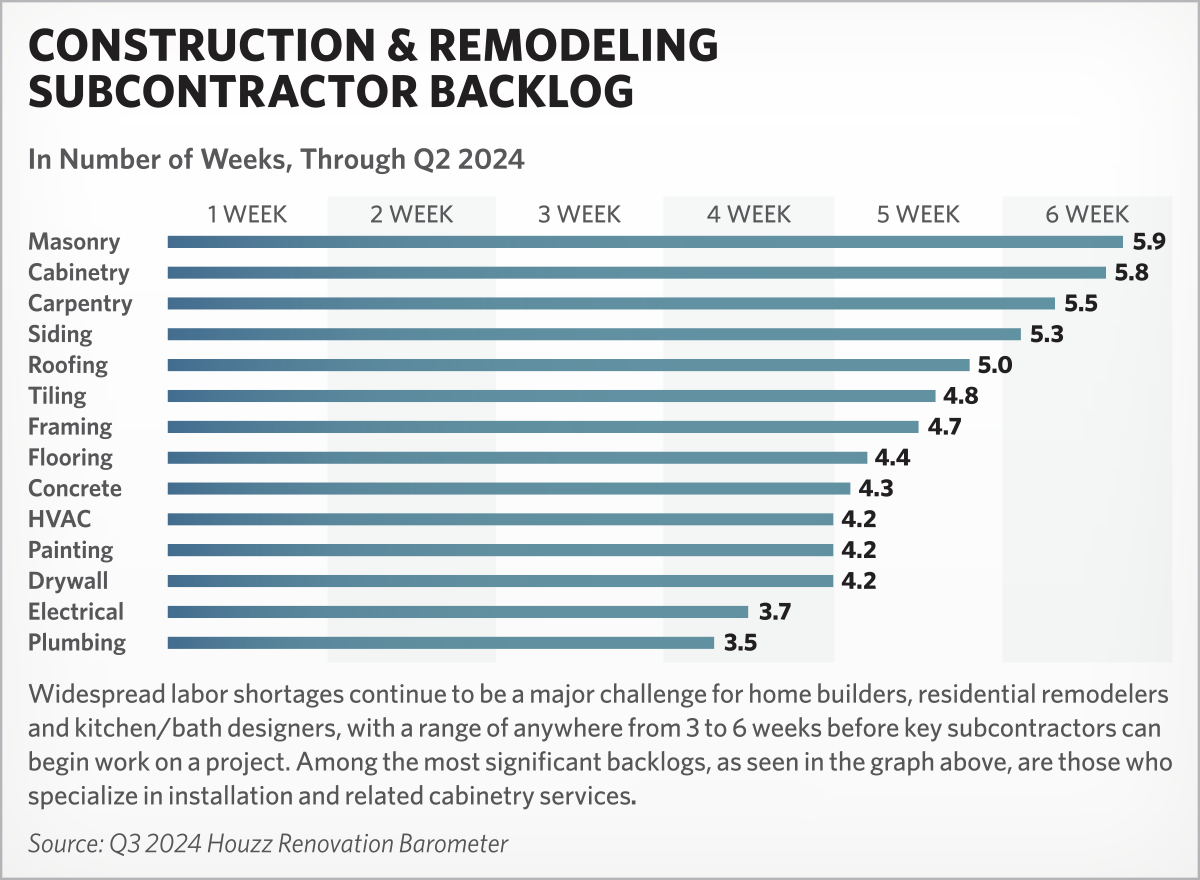

Residential Remodeling

Labor shortages continue to be a challenge for home builders, residential remodelers and kitchen/bath designers, with a range of 3 to 6 weeks before key subcontractors can begin work on a project. According to the Q3 2024 Houzz Renovation Barometer, a quarterly gauge of business conditions in the nation’s new construction and remodeling sectors, among the most significant backlogs are those in masonry, cabinetry services and carpentry (see related graph, above).“These wait times highlight the need for careful planning and coordination to ensure timely project completion,” said Marine Sargsyan, staff economist for the Palo Alto, CA-based Houzz.

Cabinet & Vanity Sales

Sales of kitchen cabinets and bathroom vanities declined in August compared to the same month a year earlier, the Kitchen Cabinet Manufacturers Association reported. According to the KCMA’s latest monthly “Trend of Business Survey,” participating manufacturers reported that overall cabinet and vanity sales were down 1.5% in August, compared to August of 2023. August sales gains were posted for semi-custom cabinets (+00.1%), as well as for custom (+1.2%). In contrast, sales of stock units declined (-9.9%). Despite the monthly gains, however, year-to-date cabinet and vanity sales through August were down 2.4% compared to the same eight-month period in 2023, the KCMA reported.